GST Registration in India 2026-27 — Complete Guide for Businesses & E-Commerce Sellers

GST Registration Services

Key Takeaways

- GST registration is mandatory above ₹40L turnover for goods, ₹20L for services, and for almost all marketplace sellers regardless of turnover.

- There is one exception — intra-state goods sellers below threshold on platforms like Meesho may be exempt since October 2023. Inter-state sellers have no such exception.

- Standard approval takes 7 working days. Low-risk applications get auto-approved in 3 days. There is also a new fast-track option from November 2025 — but it has a hidden cap that traps most growing sellers.

- TCS rate is 0.5%, not 1%. Changed in July 2024. Most guides have not updated this.

- Composition dealers cannot sell on any marketplace that collects TCS — Amazon, Flipkart, Meesho all included. This is a hard legal bar.

- FBA sellers need one GSTIN per state where Amazon warehouses their stock. A virtual office agreement (called VPOB) handles this without renting a physical office.

- Add your bank account within 30 days of getting your GSTIN. Miss this and your registration gets temporarily blocked — a trap almost no guide warns you about.

- Two-step login is mandatory from 1 April 2025. If you have not set up an authenticator app on your phone yet, you will be locked out of the GST portal.

- GST 2.0 is live from 22 September 2025. New tax slabs: 5%, 18%, and 40%. Check your product codes — several categories have been moved to different slabs.

- Aggregate turnover is calculated PAN-India — not per state, not per marketplace. One PAN, one combined number, regardless of how many states or platforms you operate in.

💡 Quick Answers

+| Question | Answer |

|---|---|

| Is GST registration mandatory? | Yes — above ₹40L for goods, ₹20L for services, and for almost all marketplace sellers regardless of turnover. |

| How long does GST registration take? | 3 working days for low-risk applications. 7 working days standard. Up to 30 days if Aadhaar verification fails. |

| What documents are needed for GST registration? | PAN, Aadhaar, photograph, address proof, bank account details, and Digital Signature for companies and LLPs. |

| Do Amazon FBA sellers need GST in every state? | Yes — one GSTIN per state where Amazon warehouses your stock. A virtual office (VPOB) agreement handles this without a physical office. |

| What is the current TCS rate for marketplace sellers? | 0.5% (0.25% CGST + 0.25% SGST) since 10 July 2024. Many guides still incorrectly say 1%. |

| Can composition dealers sell on Amazon or Flipkart? | No. The law explicitly prohibits this for any TCS-collecting marketplace. |

| Why use a service like eComHelp? | For multi-state GSTIN strategy, VPOB documentation, error-free filing, and 3-5 working day delivery — handled end to end. |

📑 Table of Contents

+- 1.What Is GST? Structure, Components & GST 2.0

- 2.Who Must Register, Thresholds & Types

- 3.GST Registration for E-Commerce Sellers

- 4.Documents Required for GST Registration

- 5.How to Register for GST: Step-by-Step

- 6.GST Registration Timeline & Fees

- 7.After Registration: The First 30 Days

- 8.GST Returns: Forms, When & How

- 9.GST Payments: How to Pay Online

- 10.Claiming Back GST (Input Tax Credit)

- 11.TCS, GSTR-8 & Marketplace Reconciliation

- 12.Composition Scheme: Should You Opt In?

- 13.GST Notices, Audits & How to Respond

- 14.Amendment, Cancellation & Suspension

- 15.What Changed Recently

- 16.Myth vs Fact: 15 Things Most Pages Get Wrong

- 17.GST Penalties & Late Fees

- 18.GST Helpline & 12-Language Support

- 19.Frequently Asked Questions

Before Amazon approves your seller account, before Flipkart lets you list a single product, before any bank opens a current account for your business, before a serious B2B buyer takes your invoice — you need a GSTIN. Which means you need GST registration. And yet, most of the guides available online are either copied from the government portal, haven't been updated since 2022, or get basic facts flat out wrong.

Over 1.5 crore businesses in India hold an active GSTIN as of 2025. If yours is not yet one of them — and you are selling on any marketplace, supplying inter-state, or earning above ₹40 lakh on goods or ₹20 lakh on services — registration is overdue.

Most GST registration guides online either copy the government portal word-for-word or still show the old 1% TCS rate from before July 2024. Many skip the most important nuance for marketplace sellers — that one GSTIN per home state is not enough if you use FBA, Smart-Fulfilment, or Quick Commerce dark stores.

This guide is different. It covers everything — who must register, the documents needed, the step-by-step process, multi-state GSTIN for marketplace sellers, return filing, TCS reconciliation, GST 2.0, and the 15 myths nearly every other guide still gets wrong. Built for first-time registrants and growing businesses alike. Not for tax consultants — for you.

1. What Is GST? Structure, Components & GST 2.0

GST stands for Goods and Services Tax. It replaced a messy combination of Central and State taxes — VAT, Service Tax, Excise Duty, and about a dozen others — when it came into effect on 1 July 2017. The idea was simple: one tax, one country, no cascading effect where you pay tax on tax on tax.

Under GST, tax is collected at every stage of the supply chain. But the tax paid at each previous stage is credited forward, so only the final consumer actually bears the full burden. For your business, this means you collect GST from your customers, subtract the GST you paid on your own purchases (called Input Tax Credit), and pay only the difference to the government.

The four components — which one applies depends on the type of sale

| Component | Full form | When it applies |

|---|---|---|

| CGST | Central GST | Intra-state sale of goods or services — Centre's share |

| SGST | State GST | Intra-state sale of goods or services — State's share |

| UTGST | Union Territory GST | Same as SGST but for union territories without their own legislature |

| IGST | Integrated GST | Inter-state sale of goods or services |

| Cess | Compensation Cess | Only on sin and luxury goods — tobacco, aerated drinks, luxury cars |

On an intra-state sale at 18%, you charge 9% CGST + 9% SGST. On an inter-state sale at 18%, you charge 18% IGST. The Centre then shares the IGST with the destination state. Your customer sees the same total tax either way.

Your GSTIN — what those 15 characters actually mean

A lot of people treat their GSTIN as just a number they paste into forms. It is worth knowing what it says about your business.

| Position | What it means | Example |

|---|---|---|

| 1–2 | State code | 27 = Maharashtra |

| 3–12 | Your PAN | ABCDE1234F |

| 13 | How many GSTINs this PAN has in this state | 1 = your first registration |

| 14 | Always Z | Z |

| 15 | Check digit (auto-calculated) | 4 |

So 27ABCDE1234F1Z4 tells you: Maharashtra-based business, PAN ABCDE1234F, first GSTIN in that state. If you open a second branch in Karnataka, your Karnataka GSTIN starts with 29.

GST 2.0 — what changed from 22 September 2025

The GST Council overhauled India's tax rate structure in September 2025 — what the industry is calling GST 2.0. The old four-slab system (5%, 12%, 18%, 28%) has moved to a cleaner three-primary-slab structure:

| Rate | What it covers |

|---|---|

| 0% | Exempt — fresh food, healthcare, education, exports |

| 5% | Essential goods and services |

| 18% | Standard goods and services — most of what you sell |

| 40% | Sin and luxury goods |

If you are an existing seller, do not assume your product's tax rate is the same as before. Several categories — personal care, certain electronics accessories, textiles — have been moved to different slabs. Check before your next return filing.

2. Who Must Register, Thresholds & Types

There are two reasons you might need to register for GST — your turnover crosses a threshold, or the nature of your business makes registration mandatory regardless of how much you earn.

Threshold-based registration

| What you sell | Most states | Special-category states |

|---|---|---|

| Goods | ₹40 lakh | ₹20 lakh |

| Services | ₹20 lakh | ₹10 lakh |

Special-category states are the northeastern states — Manipur, Meghalaya, Mizoram, Nagaland, Tripura, Arunachal Pradesh, Sikkim, Uttarakhand, Himachal Pradesh, and J&K.

One thing most people get wrong: "aggregate turnover" means all your sales combined under the same PAN — across every state, every marketplace, every product. Not per state. Not per platform. One PAN, one combined number.

Mandatory registration regardless of turnover

These businesses must register even if they earn ₹1:

- Inter-state taxable supply

- Casual taxable persons — temporary out-of-state supply (trade fairs, exhibitions)

- Persons paying GST under reverse charge

- Non-resident taxable persons

- TDS deductors

- Input Service Distributors

- E-commerce operators that collect TCS (Amazon, Flipkart, Meesho — the platforms themselves)

- Suppliers selling through e-commerce operators where TCS is collected. This is you if you sell on Amazon, Flipkart, or Meesho.

- OIDAR service providers (foreign digital services like Netflix, Google Ads)

- Online money gaming suppliers — added post-2023

The October 2023 exception

From 1 October 2023, there is one carve-out: intra-state goods sellers on certain platforms who are below the regular threshold do not have to register under the e-commerce mandatory rule. In practice, this mainly covers Meesho's intra-state seller model.

This does not apply to: service sellers, inter-state sellers, FBA sellers who warehouse in other states, or anyone who crosses the threshold. If you are on Meesho but also sell on Amazon or send packages to other states, the exemption does not protect you.

Voluntary registration — when it makes sense even below the threshold

You can register voluntarily even if your turnover is below ₹40L. Good reasons to do this: you want to claim back GST on your business purchases, your B2B buyers are asking for a tax invoice, you want to list on marketplaces that ask for a GSTIN, or you are building credibility for a bank loan application. (Worth knowing: GST registration and MSME / Udyam registration are different things — many small businesses need both.)

🎯 Do You Need GST Registration?

Three quick questions. Instant answer.

The 8 types of GST registration

| Type | Who it is for | The key thing to know |

|---|---|---|

| Regular | Most businesses | Full benefits — claim back GST on purchases, B2B invoicing, inter-state sales — no restrictions |

| Composition | Small goods businesses ≤ ₹1.5 Cr, services ≤ ₹50L | Cannot sell via marketplaces, cannot claim back GST on purchases, no inter-state |

| Casual Taxable Person | Temporary supply outside home state | Valid 90 days; pay advance tax upfront |

| Non-Resident Taxable Person | Foreign persons supplying in India | Valid 90 days; needs an Indian authorised signatory with PAN |

| Input Service Distributor | Head offices distributing GST credits to branches | Mandatory for multi-GSTIN businesses from FY 2025-26 |

| TDS Deductor | Government bodies, PSUs, notified entities | File a monthly return |

| TCS Collector / Marketplace Operator | Amazon, Flipkart, Meesho and such platforms | File a monthly return; collect TCS at 0.5% |

| OIDAR / Online Money Gaming | Foreign digital service operators | No physical place of business in India needed |

3. GST Registration for E-Commerce Sellers

This is the section most guides skip entirely or cover in two vague paragraphs. GST registration for e-commerce sellers is genuinely different from registration for an offline shop or a service business — the rules around mandatory registration, multi-state GSTINs, and marketplace compliance are specific enough that generic guides are more likely to mislead than help.

The first question: do you need one GSTIN or multiple?

This is where most new sellers go wrong. They register one GSTIN in their home state and assume that covers everything. Sometimes it does. Sometimes it really does not.

| Your situation | What you need |

|---|---|

| Single-state, you ship from home, no FBA | 1 GSTIN — your home state handles everything |

| Multi-state, courier-delivered, no warehousing | 1 GSTIN — still fine, inter-state sales handled through IGST |

| Amazon FBA with stock in 5 fulfilment centre states | 1 home GSTIN + 1 GSTIN per state where your stock sits |

| Flipkart Smart-Fulfilment in 3 states | 1 home + 3 additional state GSTINs |

| Meesho, intra-state only, below ₹40L threshold | Exempt under the October 2023 exception |

| Zepto or Blinkit with stock at their dark-store DC | 1 GSTIN per city where you stock at their DC |

The reason FBA sellers need multiple GSTINs: Amazon's Fulfilment Centres count as your "Additional Place of Business." Your stock sitting in a Karnataka FC means you are operating in Karnataka. You need a Karnataka GSTIN.

The solution for most FBA sellers is a VPOB — Virtual Place of Business. A virtual office agreement from a registered co-working or virtual office provider in the FC state gives you a legitimate business address to register. Most states accept this. A few (Tamil Nadu, Karnataka at times) have been stricter on new FBA-state registrations and may ask for physical verification.

Where every marketplace stands on GSTIN

| Marketplace | VPOB accepted? | Multi-state GSTIN needed? | What to watch |

|---|---|---|---|

| Amazon Easy Ship / Self Ship | N/A | No | Trade name on GSTIN must exactly match Seller Central |

| Amazon FBA | Yes | Yes — one per FC state | Need: VPOB agreement + provider's utility bill + NOC |

| Flipkart Self-ship | N/A | No | — |

| Flipkart Smart-Fulfilment / F-Assured | Yes | Yes — one per warehouse state | Flipkart checks that listing state matches GSTIN state |

| Meesho | N/A | No (intra-state exempt) | Goes inter-state? Register. |

| Myntra | Varies | If Myntra warehouses your stock | Brand authorisation letter needed |

| Nykaa | Varies | If Nykaa fulfills for you | Category approval is separate from GST |

| Ajio | Per Reliance norms | If Ajio warehouses | Supplier code tied to your GSTIN |

| JioMart | N/A | If hyperlocal hub-based | Food sellers need FSSAI too |

| Zepto | No — physical stock at DC | Yes — per dark-store city | Their DC = your place of business |

| Blinkit | No — physical stock at DC | Yes — per dark-store city | Same as Zepto |

Why composition dealers cannot sell on e-commerce

The law is blunt on this — a composition taxpayer cannot sell through any e-commerce operator that collects TCS. That means Amazon, Flipkart, Meesho — all of them.

You would be surprised how many guides miss this. We have seen sellers register under composition, list on Amazon, get flagged six months later, and have to retroactively migrate to regular registration while dealing with a credit mess for their buyers. Do not do this.

The fast-track registration trap — read this before you apply

To qualify, your monthly B2B output tax must not exceed ₹2.5 lakh. That is roughly ₹13.9 lakh per month in turnover at 18%. Most serious marketplace sellers cross this within 6 to 18 months of starting.

When you breach the cap, you have to file a withdrawal form within a specific window. Miss that window? Your registration becomes irregular. Every B2B buyer who claimed back the GST on purchases from you in that period faces reversal. It is a mess.

Our recommendation: If you are a marketplace seller who expects to cross ₹50 lakh per year in the next 12 months, do not opt into the fast-track option. Use the standard route — there is also a system-based 3-day approval for low-risk applications, with none of the cap restrictions.

4. Documents Required for GST Registration

Here is the thing about document rejections: they are almost never about missing documents. They are almost always about mismatched names, wrong file formats, or the address on the electricity bill not matching the address on the application. Get these details right upfront and your application sails through.

Documents everyone needs regardless of business type

- PAN card — of the business and all promoters

- Aadhaar card — of all promoters and authorised signatories

- Passport-size photograph — of each promoter and signatory

- Address proof for your principal place of business

- Bank account proof — cancelled cheque, bank statement, or passbook

- Digital Signature Certificate — mandatory for companies and LLPs; strongly recommended for everyone else

Additional documents by business type

| Type | What you need on top of the basics |

|---|---|

| Sole Proprietorship | Any government ID that links your name and address |

| Partnership Firm | Partnership Deed + firm's PAN |

| LLP | Certificate of Incorporation + LLP Agreement + LLP's PAN |

| Pvt Ltd / OPC / Public Ltd | Certificate of Incorporation + MOA + AOA + Board Resolution + company PAN |

| HUF | HUF Deed or declaration + Karta's PAN and photo |

| Trust / Society / Club | Registration Certificate + Trust Deed + governing body resolution |

| Foreign Company | Apostilled Certificate of Incorporation + Indian authorised signatory's PAN + proof of appointment |

Address proof — what works for which premises

| Your premises | What to upload |

|---|---|

| You own the place | Latest electricity bill or municipal tax receipt in your name |

| You are renting | Rent agreement + landlord's latest electricity bill |

| You are using someone else's address (consent) | NOC from the owner + owner's address proof |

| Virtual Office / VPOB | VPOB agreement + electricity bill of the VPOB provider + NOC |

| SEZ | SEZ certificate from the Development Commissioner |

Practical tips that save your application from rejection

Name the files properly — RentAgreement_Karnataka.pdf instead of scan001.jpg. The GST officer reviewing your application is looking through hundreds of submissions a day; a clearly named file signals that you know what you are doing.

Keep files under 1 MB each, in JPEG or PDF format. Anything larger gets flagged.

Make sure the name on the electricity bill matches the legal name on your PAN. This single mismatch is the reason most clarification notices are issued.

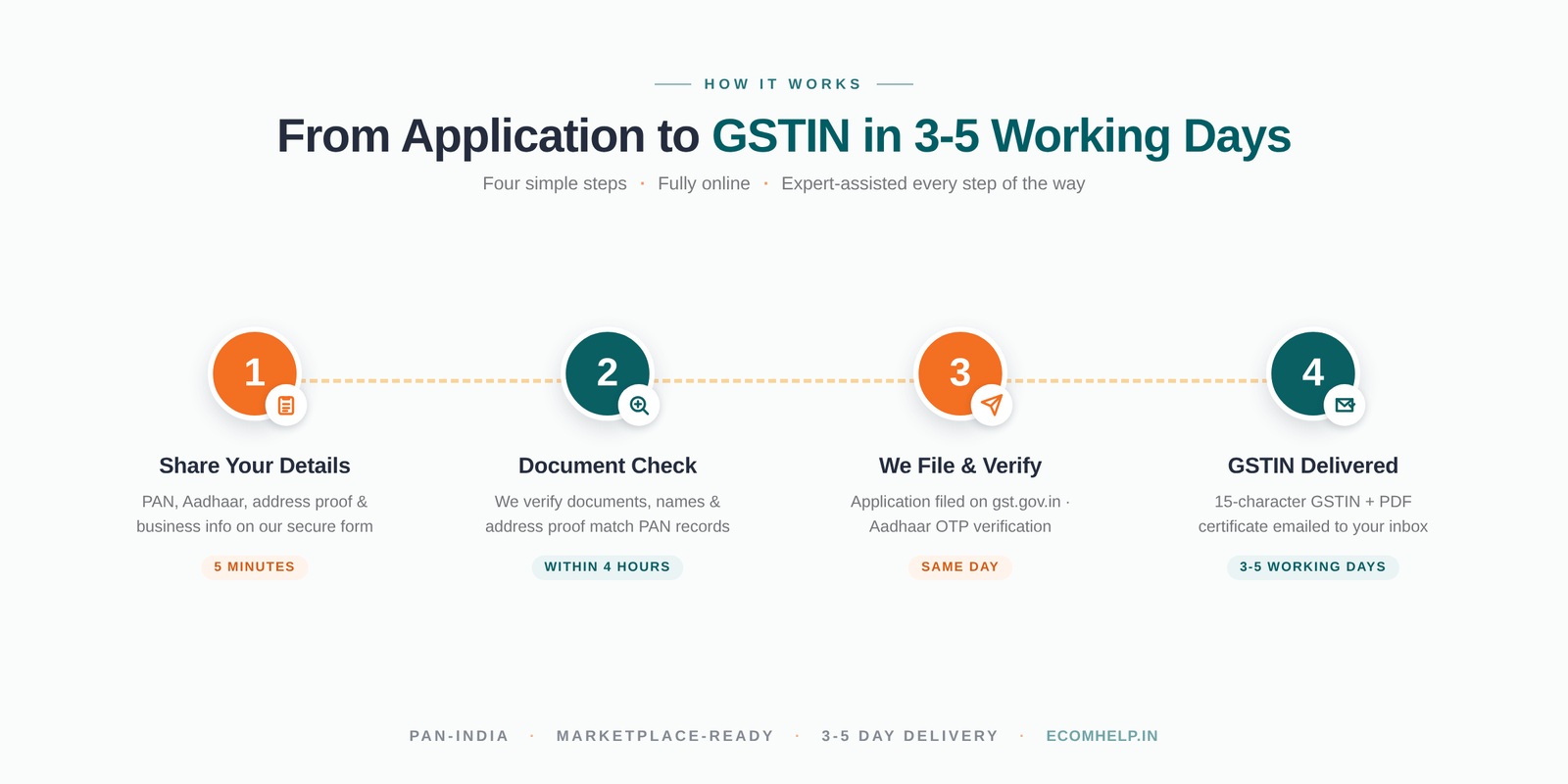

5. How to Register for GST: Step-by-Step

The GST registration process in 2025 is done entirely online at gst.gov.in — no office visit, no physical paperwork, no standing in queues. The one exception is if your state requires biometric Aadhaar verification at a GST Seva Kendra.

Part A — Get your TRN (Temporary Reference Number)

- Go to gst.gov.in → Services → Registration → New Registration

- Select your taxpayer type — Regular, Composition, NRTP, etc.

- Enter your State, District, legal name as it appears on your PAN, PAN number, email, and mobile number

- You'll get two OTPs — one on email, one on your mobile. Enter both.

- Your TRN is generated. Save it immediately. It is valid for 15 days and is not re-sent via email. If you lose it and the 15 days lapse, you start over.

Part B — Fill the registration form (10 tabs)

Log in with your TRN and work through all 10 tabs:

| Tab | What you are filling |

|---|---|

| Business Details | Trade name, business type, date you started, reason for registration |

| Promoter / Partner | Name, PAN, Aadhaar, photo — one entry per person |

| Authorised Signatory | Only if different from the promoter |

| Authorised Representative | Your CA or consultant's details — optional |

| Principal Place of Business | Full address, owned/rented/SEZ, address proof upload |

| Additional Places of Business | Every warehouse, branch, or FBA fulfilment centre state goes here |

| Goods & Services | Your top product or service codes — the system gives suggestions |

| Bank Accounts | Account number, IFSC, branch |

| State-Specific Information | Some states have additional fields |

| Verification | Sign with Digital Signature (mandatory for companies and LLPs) or e-Sign |

Aadhaar verification — OTP or biometric at a Seva Kendra?

After you submit Part B, Aadhaar verification is triggered.

If your Aadhaar is linked to your current mobile number, you get an OTP. Enter it, done.

If you are in a state that has been notified for biometric verification — Gujarat, Andhra Pradesh, Telangana, Karnataka, Maharashtra, Tamil Nadu, Delhi, and more, with rollout still ongoing — you need to visit a GST Seva Kendra in person with your original Aadhaar and PAN for biometric verification. If you skip this step, your application sits in "Pending for Aadhaar verification" indefinitely.

Two-step login — set it up before your first portal login

What happens after you submit

| Stage | How long | What is going on |

|---|---|---|

| Application submitted | Immediate | System validates the application; reference number generated |

| Auto-approval (low-risk) | 3 working days | The system processes low-risk applications automatically |

| Standard officer review | 7 working days | A GST officer manually reviews your documents |

| Clarification notice | Within 3 working days of submission | Officer needs more clarification or documents |

| Your reply | Within 7 working days of the notice | You respond with the requested documents |

| GSTIN issued | Post-approval | Certificate available to download on portal |

| Site verification | Up to 30 working days | Triggered if Aadhaar verification fails or application is flagged |

Your 7 application statuses — what each one means and what to do

| Status | What it means | Your next step |

|---|---|---|

| Pending for Processing | Application received; system or officer reviewing | Wait |

| Pending for Clarification | A clarification notice has been issued | Download the notice; reply within 7 working days |

| Clarification Filed — Pending Order | You replied; officer is reviewing your reply | Wait |

| Clarification Not Filed — Pending Order | You missed the 7-day window | Re-apply from the beginning |

| Approved | GSTIN is issued | Download certificate; set up two-step login; add bank account |

| Rejected | Application rejected | Read the rejection order carefully; re-apply with corrections |

| Withdrawn | You withdrew the application | — |

6. GST Registration Timeline & Fees

Two questions every seller asks before applying: how long does it take, and what does it cost?

How long does it actually take?

| Route | Timeline | What triggers it |

|---|---|---|

| Auto-approved (low-risk) | 3 working days | The system classifies your application as low-risk |

| Fast-track (small taxpayer opt-in) | 3 working days | You choose this scheme; B2B output tax must stay ≤ ₹2.5L per month |

| Standard with Aadhaar OTP | 7 working days | Normal applications with successful OTP verification |

| Clarification notice issued | 7 + 7 working days | Notice within 3 days; 7 days to reply |

| Site verification required | Up to 30 working days | Aadhaar verification failed or application flagged high-risk |

Cost: the official portal is free

The Government of India charges ₹0 for GST registration. Any service that adds a fee is charging for the expertise, document review, and time-saving — not for the registration itself.

eComHelp.in GST registration packages

We have helped thousands of businesses register. Here is what we offer:

| Package | Best for | What is included | Turnaround |

|---|---|---|---|

| Solo Seller | Single-state, one marketplace | Registration + GSTIN + certificate + post-registration checklist | 3-5 working days |

| Multi-State Seller | FBA / Smart-Fulfilment, up to 5 states | All registrations + virtual office documentation + state-wise compliance guide | 5–7 working days |

| Enterprise / FBA Complete | 6+ states, complex structures | Everything above + TCS reconciliation setup + ongoing support | Custom |

Get Your GSTIN in 3-5 Working Days

₹999 service fee · GSTIN delivered in 3-5 working days for eligible applicants.

Get My GSTIN →7. After Registration: The First 30 Days

Getting your GSTIN feels like the finish line. It is actually the starting line.

More compliance problems happen in the 30 days after GSTIN issuance than at any other point — because nobody tells new registrants what to do next. Here is the complete list.

Everything you need to do in the first 30 days

| When | What to do | What happens if you skip it |

|---|---|---|

| Day 1 | Download your GST registration certificate from the portal | You cannot share GSTIN proof with marketplaces or suppliers |

| Day 1 | Set up two-step login — download Google Authenticator or Microsoft Authenticator and link it to your GST login | You will be locked out of the portal on your next login |

| Day 1–3 | Link your GSTIN to every marketplace seller account you have | Listing suspension or payment hold |

| Day 1–7 | Display your GSTIN at all places of business and update it on your website | ₹25,000 penalty per instance |

| Day 1–30 | Add your bank account details on the portal | Your GSTIN gets temporarily blocked |

| Day 1–30 | Start issuing GST-compliant tax invoices — legal name, GSTIN, product code, correct tax split | Your buyers cannot claim back the GST on purchases from you |

| Before first return | Set your return filing preference — monthly or quarterly | Wrong filing frequency, late fee risk |

The bank account deadline — this one bites people

A blocked GSTIN cannot issue valid tax invoices, generate e-way bills, or file returns. Reviving it requires filing a revival form and waiting for officer review. This is a completely avoidable problem. Set a calendar reminder the minute you get your GSTIN.

The 10-field address on your certificate — verify it carefully

The new GST registration certificate uses a 10-field address format: Floor No. → Building Name → Premises Name → Road/Street → Landmark → Locality → City → District → State → PIN. Go through every field and make sure it matches your actual address before you start distributing the certificate to suppliers and buyers. One mismatch can create credit disputes during audits.

8. GST Returns: Forms, When & How

Once registered, you are on a GST return filing calendar whether you are selling or not. Even if you do zero business in a month, you file a nil return. Miss it and the late fee clock starts ticking immediately.

The full GST returns calendar

| Return | Who files it | What it covers | How often | Due date |

|---|---|---|---|---|

| GSTR-1 | Regular taxpayers | Your sales (outward supplies) | Monthly or Quarterly | 11th / 13th |

| GSTR-3B | Regular taxpayers | Tax payment summary | Monthly or Quarterly | 20th / 22nd / 24th (state-wise) |

| GSTR-8 | E-commerce operators | TCS collected from sellers | Monthly | 10th |

| GSTR-9 | All regular taxpayers | Annual reconciliation | Annual | 31 December |

| GSTR-9C | Turnover > ₹5 Cr | Audited reconciliation | Annual | 31 December |

| CMP-08 | Composition taxpayers | Quarterly tax payment | Quarterly | 18th of month after quarter |

| GSTR-4 | Composition taxpayers | Annual return | Annual | 30 April |

| GSTR-7 | TDS deductors | TDS deducted | Monthly | 10th |

Quarterly filing — a simpler option if your turnover is below ₹5 crore

The QRMP scheme (Quarterly Return Monthly Payment) lets you file GSTR-1 and GSTR-3B quarterly instead of monthly. You still pay tax monthly through a challan, but the return filing burden drops significantly. Most small and medium sellers do well on QRMP.

The nil return late fee myth — still showing up on guides in 2025

Almost every guide online says nil returns have no late fee. This has not been true for years. GSTR-3B late fee is ₹20 per day even for nil returns (₹10 CGST + ₹10 SGST). Not a huge amount per day — but if you miss 3 months on two returns, you are looking at ₹3,600 in late fees before interest. File on time, every time.

9. GST Payments: How to Pay Online

When it is time to pay your GST, everything happens through the portal. There are no cheques, no physical bank visits needed (unless you specifically prefer paying at a bank counter).

The three ledgers — think of these as three buckets

| Ledger | What sits in it | When it is used |

|---|---|---|

| Liability Ledger | The tax you owe (from your GSTR-3B) | Must be cleared using one of the other two |

| Credit Ledger | GST you have accumulated from purchases | Used first — must be exhausted before touching cash |

| Cash Ledger | Cash you deposit + TCS received from marketplaces | Used after the credit is exhausted |

The system forces a specific order: credit first, then cash. You cannot skip this.

How to make a GST payment

- Go to gst.gov.in → Services → Payments → Create Challan

- Enter amounts by head — IGST, CGST, SGST, Cess separately

- Choose your payment mode: Net Banking, NEFT/RTGS, Debit Card, or at a bank counter

- After payment, the amount reflects in your Cash Ledger within one working day

- When you file GSTR-3B, the system auto-offsets credit first, then uses your Cash Ledger

Interest on late or short payment: 18% per annum. There is no grace period — it starts the day after the due date. On a ₹1 lakh underpayment, that is ₹49 per day in interest.

10. Claiming Back GST (Input Tax Credit)

This is the mechanism that makes GST non-cascading — you subtract the GST you paid on your inputs from the GST you collect on your outputs, and only pay the government the difference. In practice, it means every GST rupee you paid on raw materials, packaging, shipping, and services can come back to you.

Four conditions — all four must be met to claim it

- You hold a valid tax invoice from a GST-registered supplier

- You have actually received the goods or services

- The supplier has paid the tax and filed their return — meaning it shows up in your monthly statement (GSTR-2B)

- You have filed your own GSTR-3B

If your supplier files late or does not file at all, condition 3 fails and you cannot claim that credit — even if you have a perfect invoice in hand. This is why chasing suppliers to file on time is genuinely in your financial interest.

Credit you cannot claim

The law blocks the credit on a specific list: personal-use motor vehicles, food and beverages (unless you are in the food business), outdoor catering, health clubs, beauty treatments, club memberships, construction of personal/immovable property, and life/health insurance for employees (unless mandated by law).

GSTR-2B is your only source of truth

Your monthly GSTR-2B statement is auto-populated from your suppliers' filings. Claim only what is in GSTR-2B. If something is missing, the supplier has not filed — follow up with them directly. Mismatches between your claim and your GSTR-2B are one of the most common triggers for GST scrutiny notices.

11. TCS, GSTR-8 & Marketplace Reconciliation

This is the section most specific to marketplace sellers — and almost entirely absent from every other guide. Here is exactly how TCS works, where the money goes, and how to make sure you are not leaving credit on the table.

TCS — what it is and what the current rate is

Every marketplace operating in India must deduct Tax Collected at Source (TCS) from your settlement and deposit it with the government. The rate from 10 July 2024 is:

- 0.5% of your net taxable sales value — not the total invoice, just the taxable portion before GST

- Split as 0.25% CGST + 0.25% SGST on intra-state supplies

- Or 0.5% IGST on inter-state supplies

The old rate was 1%. Most guides still say 1%. If your marketplace is still deducting at 1%, raise a ticket immediately — that is your money.

How TCS flows from the marketplace to your GST credit

Walk through a real example. You make a ₹10,000 sale. Taxable value: ₹8,475. GST at 18%: ₹1,525.

- Marketplace deducts TCS: 0.5% × ₹8,475 = ₹42.38 held back from your payout

- Marketplace deposits ₹42.38 with the government and files its monthly TCS return by the 10th of the following month

- ₹42.38 auto-populates in your monthly GSTR-2B statement as TCS credit received

- This credit moves to your Cash Ledger

- When you file GSTR-3B, your output GST liability (say ₹1,525) is offset first by your purchase credits, then by your Cash Ledger balance — which includes this TCS credit

- You pay only the net remaining balance in cash

GST TCS vs Income Tax TDS — keep these completely separate

Both apply to marketplace sellers. They are from two different tax systems and cannot be offset against each other.

| GST TCS | Income Tax TDS | |

|---|---|---|

| Rate | 0.5% of net taxable value | 1% of gross sale value |

| Marketplace files | Monthly TCS return on GST portal | Quarterly TDS return on Income Tax portal |

| Shows up in your | Monthly GSTR-2B → Cash Ledger | Form 26AS / AIS |

| Offset against | Your GST output tax liability | Your Income Tax advance tax |

Section 9(5) — when the marketplace pays GST on your behalf

For certain specified services, the law makes the marketplace pay the GST directly — not you. This applies to:

| Service | Platform | What it means for you |

|---|---|---|

| Cab / auto / taxi rides | Ola, Uber, Rapido | Driver does not charge or collect GST on app rides |

| Restaurant food delivery | Swiggy, Zomato | Platform pays GST; restaurant does not charge separately on app orders |

| Housekeeping, plumbing, carpentry | UrbanCompany | Platform pays GST; individual provider does not collect |

| Small hotel / homestay (below threshold) | Booking.com, MakeMyTrip | Platform pays GST; host does not charge separately |

The important caveat: this only covers the supplies made through that platform. If the same restaurant earns from dine-in, direct orders, or catering — and total turnover crosses ₹20 lakh — it must register and charge GST on those other supplies.

12. Composition Scheme: Should You Opt In?

The Composition Scheme exists for small businesses that want simplicity over sophistication — a flat rate on turnover, quarterly returns, no input tax credit calculation. For the right business, it is genuinely useful. For the wrong business, it is a serious mistake.

Who can opt in — and at what rate

| Business type | Turnover limit | Tax rate on turnover |

|---|---|---|

| Manufacturers | ₹1.5 crore (₹75L in special states) | 1% |

| Traders (goods resellers) | ₹1.5 crore (₹75L in special states) | 1% |

| Restaurants — no alcohol served | ₹1.5 crore (₹75L in special states) | 5% |

| Service providers | ₹50 lakh | 6% |

What being on composition actually means

You pay GST on your total turnover at the flat rate above — not just on your margin, not after deducting credits. You issue a "Bill of Supply" instead of a tax invoice. Your buyers cannot claim back the GST from you. You cannot sell inter-state. You file simpler quarterly and annual returns.

Who should choose composition

A local kirana store selling only within their city. A neighbourhood restaurant. A small service provider with entirely local, face-to-face, B2C customers who have no use for input tax credit and want minimal compliance.

Who should absolutely not choose composition

Anyone selling on Amazon, Flipkart, Meesho, or any marketplace — the law prohibits this, period. Anyone selling inter-state. Anyone whose buyers are GST-registered businesses that need to claim back the GST from your invoice. Anyone who expects to grow beyond the threshold in the next year.

If you are an e-commerce seller considering composition because "it seems simpler" — the answer is no. Register as Regular from day one. Composition will cost you more in lost credits and the eventual forced migration than the compliance simplification saves you.

13. GST Notices, Audits & How to Respond

Receiving a GST notice does not mean you have done something wrong. It means a system or an officer has flagged something that needs a response. The worst thing you can do with any GST notice is ignore it.

The most common notices and what they mean

| Notice | What it means | Your window |

|---|---|---|

| Registration Clarification | Officer needs more info during your registration | 7 working days |

| Return Scrutiny | Discrepancy found in your returns | 30 days |

| Audit Notice | Physical audit of your records | 15 days prior notice |

| Demand Notice — Non-fraud | Tax demand without allegations of fraud | Show cause + adjudication |

| Demand Notice — Fraud | Tax demand where deliberate evasion is alleged | Show cause + adjudication |

| Cancellation Notice | Officer is proposing to cancel your registration | 7 working days |

The only rule you need to remember about GST notices

Download it from the portal the day it arrives. GST notices are not always emailed — they are posted to your portal dashboard. Check your dashboard every week, not just when you are filing. Note the response deadline. Respond before it. Even if you need more time, an acknowledgement and a request for extension is infinitely better than silence.

If you do not respond, the officer can issue what is called a "best judgement assessment" — they decide the tax amount themselves, usually higher than what you actually owe.

14. Amendment, Cancellation & Suspension

Core vs non-core amendments — two very different processes

| Type | Examples | How to do it | How long |

|---|---|---|---|

| Core — officer approval needed | Legal name change, principal address change, add or remove a promoter | File the amendment form; officer reviews | Up to 15 working days |

| Non-core — immediate | Mobile number, email, bank account, additional place of business | Update on the portal directly | Immediate |

The PAN portability trap — a mistake that creates massive problems

If your PAN changes — because you converted from sole proprietorship to a company, or because of a business restructuring — you cannot amend your GSTIN. You must cancel the existing GSTIN and apply fresh under the new PAN.

Same with state: if you move your business from Maharashtra to Karnataka, you cannot amend the Maharashtra GSTIN to a Karnataka one. Cancel in Maharashtra (after clearing all returns and dues) and register fresh in Karnataka.

The danger here: businesses that try to amend these fields when fresh registration is the correct path end up with irregular GSTINs. Every B2B buyer who has claimed back the GST on invoices from you then faces reversal.

Cancellation

You can voluntarily cancel when: business is shut down, transferred, amalgamated, or turnover has been below threshold for 12 consecutive months. Before you apply, file every pending return — GSTR-1, GSTR-3B, GSTR-9. A cancellation with pending returns will not go through.

Suspension — what triggers it automatically

- Returns not filed for 6 consecutive months (regular) or 3 consecutive quarters (composition)

- Bank account not added within 30 days of GSTIN

- Significant GSTR-1 vs GSTR-3B discrepancies flagged by the system

How to revive: File all pending returns → apply for revocation → officer reviews and revokes suspension.

15. What Changed Recently — A Quick Update

GST is not a set-it-and-forget-it compliance. Seven material changes in the last 18 months alone.

| Date | What changed | What it means for you |

|---|---|---|

| 10 Jul 2024 | TCS rate cut to 0.5% (from 1%) | Your marketplace deductions halved; check all settlement statements from July 2024 onwards |

| 1 Apr 2025 | Two-step login mandatory for all GST portal logins | Set up an authenticator app before your next login or you will be locked out |

| Apr 2025 | Biometric Aadhaar at Seva Kendras — pan-India rollout | New registrations in notified states require in-person visit |

| 22 Sep 2025 | GST 2.0 — new tax slabs (5%, 18%, 40%) | Verify your product codes; several categories reclassified |

| 1 Nov 2025 | New fast-track 3-day registration option | Available but has a ₹2.5L per month B2B output cap — not right for most marketplace sellers |

| 1 Nov 2025 | System-based 3-day approval for low-risk applications | Low-risk applications still get 3-day auto-approval — this is the right route for most sellers |

| Nov 2025 | Bank account 30-day deadline reaffirmed | Not adding bank account within 30 days of GSTIN now triggers automatic suspension |

16. Myth vs Fact: 15 Things Most Pages Get Wrong

We went through 75+ GST registration guides — from the big-name service firms to the bank blogs to the marketplace seller pages. These 15 errors showed up over and over. Every single one has a real consequence for businesses that believed it.

| # | What most pages say | What is actually correct |

|---|---|---|

| 1 | "Threshold for goods is ₹20 lakh" | ₹40 lakh in most states since 1 April 2019 |

| 2 | "TCS rate is 1%" | 0.5% total (0.25% + 0.25%) from 10 July 2024 |

| 3 | "Composition limit is ₹1 crore" | ₹1.5 crore for goods; ₹50 lakh for services |

| 4 | "Registration takes 30 working days" | 3 days for low-risk; 7 days standard; 30 days only if Aadhaar verification fails |

| 5 | "All e-commerce sellers mandatory regardless of turnover" | Intra-state goods sellers below threshold on qualifying platforms are exempt since Oct 2023 |

| 6 | "Government fee is ₹100 or ₹500" | The official portal charges nothing — third parties charge service fees |

| 7 | "Composition dealers can sell on Amazon or Flipkart" | Explicitly prohibited. Hard legal bar. |

| 8 | "Aadhaar verification is optional" | Mandatory since 1 January 2022; biometric at Seva Kendras in notified states from 2025 |

| 9 | "Aggregate turnover is calculated per state" | PAN-India across all GSTINs under the same PAN |

| 10 | "GST certificate is valid for 1 year" | Indefinite for regular taxpayers; 90 days for casual / non-resident taxable persons |

| 11 | "No late fee for nil GSTR-3B" | ₹20 per day late fee even on nil returns |

| 12 | "ARN and GSTIN are the same" | ARN is the application reference (issued at submission); GSTIN is the tax ID (issued on approval) |

| 13 | "Changing your address means you amend your GST" | Intra-state address: amend through the form. Change of state or PAN: fresh registration required |

| 14 | "Bank account can be added whenever" | Mandatory within 30 days; delay triggers automatic suspension |

| 15 | "Section 24 makes all e-commerce mandatory" | One section covers sellers; another covers operators. Different provisions, different consequences |

17. GST Penalties & Late Fees

Nobody likes this section. But knowing these numbers in advance is the cheapest compliance insurance you can get.

| What you did | Penalty |

|---|---|

| Did not register when mandatory | ₹10,000 or 10% of tax due — whichever is higher |

| Wilful tax evasion | 100% of tax evaded + 1–5 years imprisonment |

| GSTR-1 filed late | ₹50 per day (₹20 per day for nil); capped at ₹5,000 |

| GSTR-3B filed late | ₹50 per day (₹20 per day for nil); capped at ₹10,000 |

| GSTR-9 annual return filed late | ₹200 per day; capped at 0.5% of turnover |

| Tax paid late | 18% per annum interest from the due date |

| Excess credit claimed | 24% per annum interest |

| GSTIN not displayed at premises | ₹25,000 per instance |

One thing worth calculating: ₹50 per day across two returns (GSTR-1 + GSTR-3B) is ₹100 per day, ₹3,000 per month. If you miss three months, that is ₹9,000 in late fees before interest even begins. Set automated reminders. File on time. Always.

18. GST Helpline & 12-Language Support

When something goes wrong — application stuck, GSTIN suspended without warning, portal error you cannot resolve, notice in confusing language — here is exactly where to go. This information is buried in the official GST Welcome Kit. Almost no public guide mentions it.

The official self-service grievance portal — selfservice.gstsystem.in

This is the official portal for taxpayers. You can report:

- Registration issues — application stuck, ARN error, biometric failure

- Return filing issues — GSTR-1 upload error, GSTR-3B mismatch

- Payment issues — challan generated but amount not credited to your ledger

It is available in 12 Indian languages: English, Hindi, Bengali, Marathi, Telugu, Tamil, Gujarati, Kannada, Odia, Malayalam, Punjabi, and Assamese. Select your language from the dropdown when filing a complaint. No guide on the internet highlights this — but it is real government-built infrastructure that resolves most portal-level issues within 2–5 working days.

Other support channels

| Channel | Contact | Hours |

|---|---|---|

| CBIC Toll-Free | 1800-103-4786 | 9 AM – 7 PM, Mon–Sat |

| GSTN Helpdesk | 0120-4888999 | Business hours |

| Online Chat | gst.gov.in → Help → Chat | Portal hours |

| GST Seva Kendra | Check gst.gov.in for state-wise locations | Varies |

19. Frequently Asked Questions

Register Your GST with eComHelp

We have helped thousands of businesses and e-commerce sellers across India get their GSTIN — with expert review on every application and a 3-5 working day turnaround for eligible applicants. Whether you are registering for the first time, adding multi-state GSTINs, or amending your existing registration — our team handles it end to end.

Get Your GSTIN in 3-5 Working Days

₹999 service fee · GSTIN delivered in 3-5 working days for eligible applicants.

Get My GSTIN →📚 References

+For readers who want to verify the details cited in this guide, here are the source documents:

- CGST Act 2017 (as amended) — primary law governing GST in India

- CGST Act — Section 2(6) — definition of aggregate turnover

- CGST Act — Section 9(3) — reverse charge mechanism

- CGST Act — Section 9(5) — deeming fiction for marketplace services

- CGST Act — Section 10(2)(d) — composition scheme bar on e-commerce

- CGST Act — Section 16 — input tax credit eligibility

- CGST Act — Section 17(5) — blocked input tax credits

- CGST Act — Section 22 — threshold-based registration

- CGST Act — Section 24(ix), (x) — mandatory registration for e-commerce

- CGST Act — Section 25 — registration procedure

- CGST Act — Section 47 — late fee

- CGST Act — Section 50 — interest on late payment

- CGST Act — Section 52 — TCS provisions

- CGST Act — Sections 73, 74 — demand notices

- CGST Act — Section 122 — general penalties

- CGST Act — Section 132 — imprisonment for fraud

- CGST Rules — Rule 8(4A) — biometric Aadhaar at Seva Kendras

- CGST Rules — Rule 9 — standard registration timeline

- CGST Rules — Rule 9A — risk-based 3-day auto-approval

- CGST Rules — Rule 10A — bank account 30-day deadline

- CGST Rules — Rule 14A — Simplified Registration Scheme

- CGST Rules — Rule 21A — automatic suspension triggers

- Notification 10/2019-CT — ₹40 lakh threshold for goods

- Notification 15/2024-CT — TCS rate reduced to 0.5%, effective 10 July 2024

- Notification 18/2025-CT — Fast-track registration scheme (Rule 14A), effective 1 November 2025

- Notification 34/2023-CT — intra-state e-commerce seller exemption, effective 1 October 2023

- Notification 38/2021-CT — Aadhaar authentication mandatory

- Notification 76/2018-CT — late fee provisions

- 56th GST Council Recommendations (September 2025) — GST 2.0 rate restructuring

- GSTN Advisory March 2025 — two-step login mandatory

- GSTN Advisory November 2025 — bank account suspension under Rule 10A